You may have heard about a reverse mortgage, but many people don't know anything about what they do or who should consider using them. In this article, we will answer your question of how does a reverse mortgage work.

While there are obviously many different kinds of loans you could use, once we answer the question "How does a reverse mortgage work?", you will see the advantages and disadvantages and be able to determine if it is the right option for you and your situation.

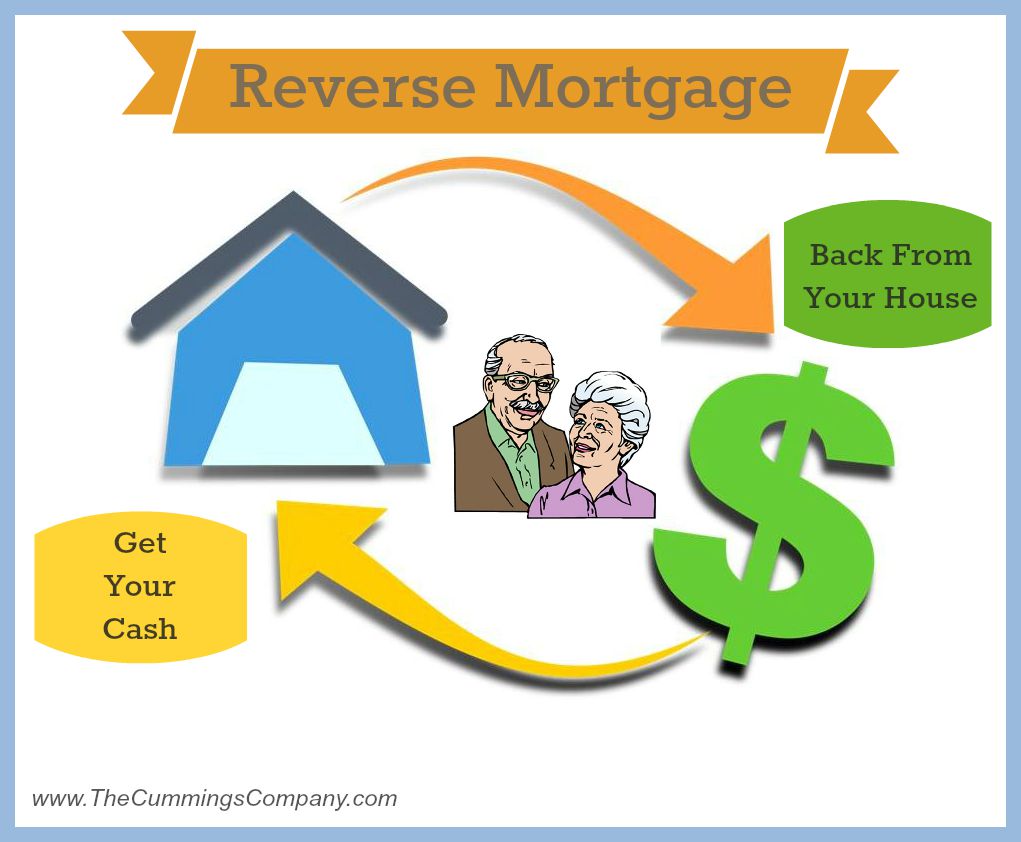

How Does a Reverse Mortgage Work?

Photo credit by: reverse.mortgage.com

You probably know that a Reverse Mortgage uses your home’s equity as collateral. You have been living at your home for quite some time, so you know you would qualify for a good amount that would serve you well at this point in your life. However, you have your doubts. Your home is the largest asset you own, and you don’t want to do anything to put it at risk. But wait, if you take out a reverse mortgage, would you be incurring a risk? How does a reverse mortgage work? Let’s review the scenario and get some questions answered.

Why Not Simply Get a Home Equity Loan?

Generally, a Home Equity Loan has strict requirements regarding income and creditworthiness. Also, you must make monthly payments to repay the loan. In contrast, in the case of a reverse mortgage, the amount that can be borrowed is determined by using a formula that takes into account current interest rates and the appraised value of the property in question. No monthly payments need to be made as long as you live in the home and keep up the payments of property taxes, insurance, and maintenance.

What Is a Reverse Mortgage?

A reverse mortgage is also referred to as a home equity conversion mortgage. This is a financial product available to homeowners who are 62 years old or older, who have accrued substantial home equity and are interested in obtaining these funds in order to supplement their retirement income. What makes this product so attractive is the fact that, as opposed to a conventional forward mortgage, there are no monthly mortgage payments to make in this case. However, you must keep in mind that if you obtain a reverse mortgage, you are still responsible for paying taxes and insurance on the property, and you must continue to consider this home as your primary residence for the duration of the loan.

How Does a Reverse Mortgage Work?

In a traditional mortgage, you, as the borrower, must make monthly payments to the lender. This results in a gradual reduction of the loan balance, and this is how you build equity. When it comes to a reverse mortgage, you receive payments from the lender and do not need to pay these funds back so long as you continue living in the home and continue to fulfill your basic responsibilities, as stated above. The loan balance grows over time as you receive the payments and interest accrues on the loan; home equity is reduced over time. How does a reverse mortgage work? Basically, the mortgage works in the reverse direction of a traditional mortgage which is why it is known as a “reverse” mortgage.

It comes as no surprise to anyone that all loans must eventually be repaid. In this case, how does a reverse mortgage work? In a reverse mortgage, the loan is due, and the mortgage is paid off once you either sell the home or pass away. You may also decide to pay off the loan at any time. It is important to understand that reverse mortgages are designed in such a way that the amount owed cannot exceed the value of the home.

How does a reverse mortgage work? Here is an interesting example: let's say that a reverse mortgage balance is $250,000, and the house is sold for $225,000. In this case, the borrower does not owe the difference. On the other hand, if the house is sold for more than the value of the reverse mortgage, the equity belongs to either the borrower or the borrower’s estate, as the case may be.

Who May Qualify for a Reverse Mortgage?

The Federal Housing Administration specifies that all homeowners need to be at least 62 years old to qualify for this financial product. Additionally, the home must be completely paid up or you may use some of the money to pay it off. It is interesting to note that there are no credit scores required for this transaction.

Here are the basic requirements you must meet in order to qualify for this type of mortgage:

It is also a requirement that you meet with an HUD-approved counselor to determine if the product is what you are looking for and will satisfy your needs. These sessions should help you answer all questions relating to how does a reverse mortgage work and what options are available. If you are considering this type of loan, you must also undergo a financial assessment to qualify for it.

How Much Money Can You Get?

There are four factors that determine the amount you are eligible to receive when applying for a reverse mortgage:

Do You Need to Receive All the Money at Once?

In this case, the answer is no. You can choose between a lump sum at closing, receiving monthly payments as long as you live in the home, getting payments during a certain number of years, a line of credit from which you can draw at any time until the credit is exhausted, or a combination of the above.

Your choice as to how to get the money is important. Here are the options available to you when you receive a reverse mortgage:

Opt for a Lump Sum

The simplest and most straightforward option is to get all the money at once. If this is the option you select, your loan will have a fixed interest rate, and the loan balance will grow over time as interest accrues.

Opt to Receive Periodic Payments

You can also select to obtain regular payments—monthly, for example. Payments can last for your entire life, or for an established length of time, such as 10 years. If your loan becomes due because all borrowers have moved out, the payments end. With lifetime payments, it’s possible to take out more than you and your lender predicted if you live a very long life.

Select a Line of Credit

Instead of receiving the cash right away, a line of credit allows you to draw funds when you need them. The advantage here is that you only pay interest on the money you actually borrow, and your credit line might grow over time.

Go for a Combination

If you can’t decide, you may use a combination of the options described above.

When Do You Have to Start Paying Back a Reverse Mortgage?

As long as at least one of the property owners continues to live full-time in that property and continues to make the necessary payments (mainly taxes and insurance), the mortgage does not become due.

What Happens After the Homeowners Pass Away?

When the homeowners pass away, the estate can decide whether to repay the mortgage or put the home up for sale. If the equity in the home is higher than the balance of the loan when the home is sold to repay the loan, the remaining equity belongs to the estate. No assets are affected by a reverse mortgage, no investments, other properties, car or valuables can be taken to pay off the reverse mortgage.

Conclusion

If you are considering applying for a reverse mortgage, don't sign on the dotted line before you take the time to talk to your lender about the fees associated with this type of financial product. They may be too high for your comfort. Also, consider the fact that, in general terms, the interest rate on a reverse mortgage is higher than that of a traditional home equity loan. Make sure you understand clearly the costs associated with the reverse mortgage before committing to it.

Remember, you do not have to repay the loan as long as you continue living in the property as your primary residence. However, life happens and it may be that you need or want to move out of this house. What happens if you have to move out, let’s say, to a long-term care facility? You will have to start repaying the mortgage at a time when money might be tight.

Finally, there is the subject of inheritance. If this home has been in your family for decades and you dream about your children living there after you die, you can forget about that dream if you have a reverse mortgage. As mentioned above, the house needs to be sold to repay the mortgage. If this is your wish, a reverse mortgage might not be for you.

Leave a Reply